Table of Contents

Quick overview of IRA types

Part 1: IRAs

Part 2: 401(k), 403(b), and 529 Plans

Part 3: 529 Plan: Rules & Requirements

Part 4: Retirement Advice for Women Investors

Congratulations! If you’ve read this far, you get a free IRA!

What is an IRA?

An individual retirement account (IRA) is a tax-advantaged way for individuals to save for retirement. An IRA itself is not an investment – rather, it’s a type of account that contains investments in the form of stocks, bonds, mutual funds, etc.

And it’s becoming more important to American workers. Twenty years ago, assets in IRAs made up just 21 percent of our retirement savings. Today, IRA funds make up more than a third of that savings, or $9.3 trillion.

Why the increase in popularity?

The landscape of American work and retirement savings is changing. Employees today are more likely to hop from job to job, which makes an IRA an attractive investment tool: unlike a 401(k), it’s not tied to an employer.

And employer-sponsored retirement vehicles themselves may be harder to come by. With the rise of the “gig economy,” more workers than ever are freelancing or contracting, meaning they have to create benefits like retirement accounts on their own – which is exactly what the IRA enables.

Even as IRAs are becoming more relevant than ever, though, as many as 45 percent of people think they’re too complicated to understand. Considering nearly four out of five of us are at least somewhat concerned that we won’t have enough money for retirement – and 21 percent of us have nothing at all saved for retirement – it’s time to bridge the knowledge gap.

One more thing: there’s a good chance that Social Security won’t be as robust in the future as it is now, which means that now is the time to learn everything you can about IRAs to set yourself up for a successful and well-funded retirement.

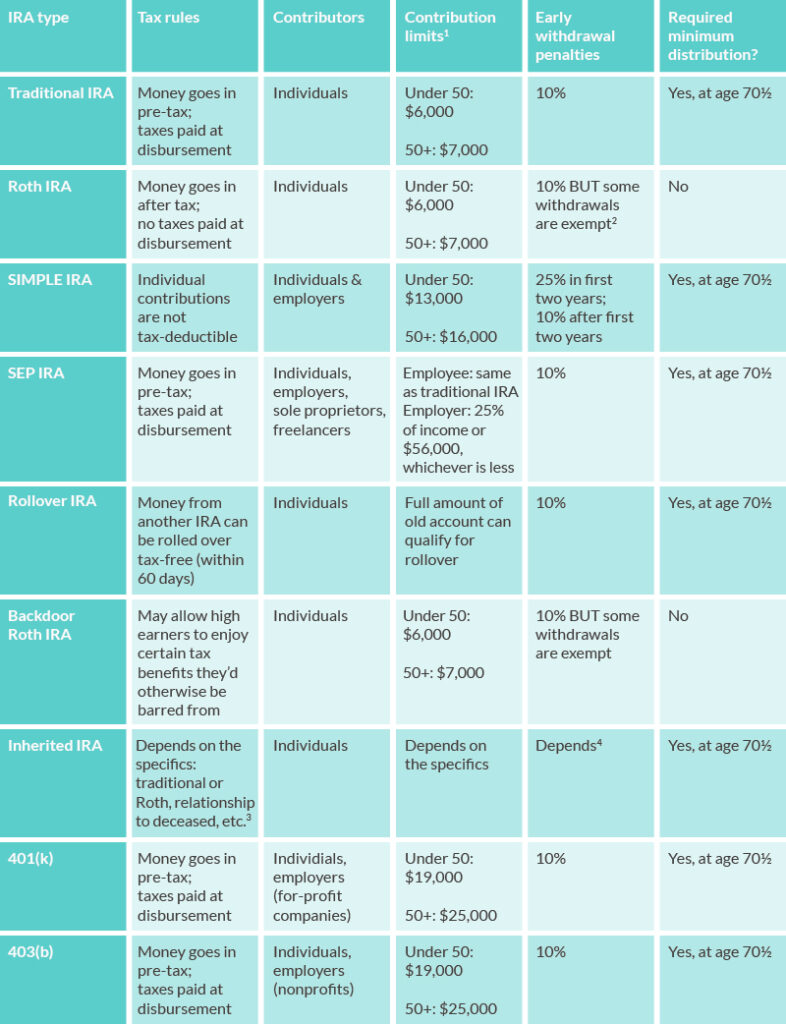

Quick overview of IRA types

As you’ll see in this guide, there are several IRA types, each with its own set of rules. We’ll get into the details of each below, but here’s a quick guide to how each IRA type works so you can start to get a sense of which IRA might be best for you.

Individual Retirement Account

Ever found yourself wondering “What is an IRA?” Considering opening an IRA as part of your retirement planning, but don’t know how an IRA works? Don’t know the difference between the various types of IRA? Worried about IRA fees? What about all those confusing IRA rules? Never fear. This guide will outline the basics to help you understand which IRA is best for you. You’ll be breezing through discussions of “traditional vs. Roth” IRAs in no time.

Part 1: IRAs

How does an IRA work?

As with most things financial, there are a lot of rules governing how IRAs work. Here are the basics:

- You open an IRA when you’re earning money.

- You contribute earned income to an IRA (regardless of type) during your working years.

- Those contributions are invested in various ways with the goal of earning money.

- Those earnings are reinvested, compounding the benefit.

- Depending on the type of IRA, you money is taxed before it enters the account or when it leaves. It is not taxed while in the IRA, giving you tax-free growth.

- You withdraw funds from the IRA when you retire, to replace your income.

There are annual limits on how much money you can contribute to your IRA. There are also a lot of rules about when you can or must take money out (distributions) and how much you can or must take out when you do. But the basic concept is the same regardless of the type of IRA you choose – Roth, SIMPLE, SEP, or traditional IRA.

What IRA types are there?

There are several types of IRAs:

- Traditional IRA

- Roth IRA

- SIMPLE IRA

- SEP IRA

- Rollover IRA

Though there are similarities, each IRA type has a different set of rules covering how it’s funded, taxed and penalized, and how you get money out. Because of that, there’s no single “best IRA.” The best IRA for you depends on your needs, current income, retirement plans, age, and more. Let’s take a look at each IRA type.

Traditional IRA: Rules & age requirements

What is a traditional IRA?

The traditional IRA is a type of IRA that almost any employed person can open. If you’re under 50, your contributions to a traditional IRA may be tax deductible up to $6,000 annually as of 2019. Whether contributions are tax deductible, and how much you may deduct, is determined by several factors:

- Your filing status (single, married filing jointly, etc.).

- Whether you’re covered under an employer-sponsored retirement plan.

- Your MAGI (Modified Adjusted Gross Income).

IRA tax-deductible contributions

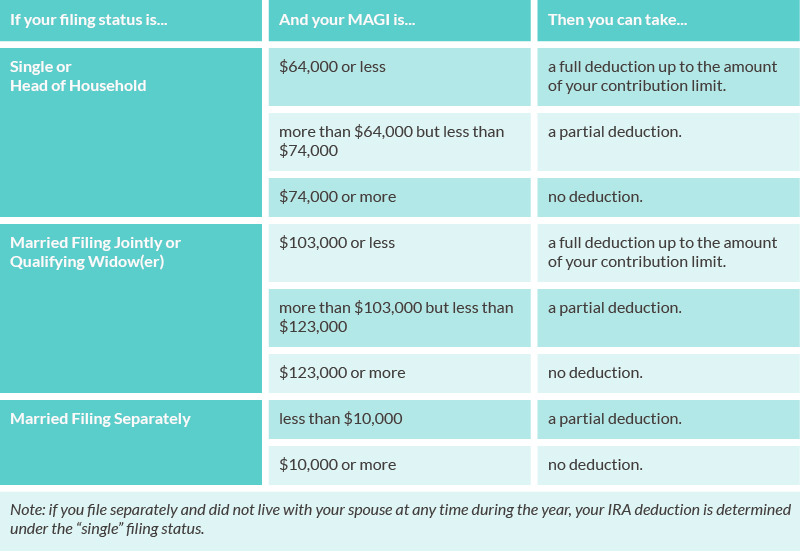

If you are covered under an employer-sponsored retirement plan, you can determine how much of your IRA contribution is tax deductible based on your MAGI. Use the rules in this table to get an idea:

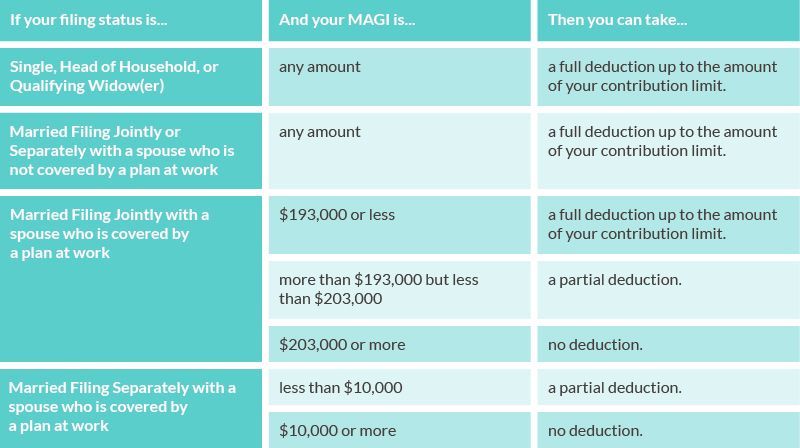

If you are not covered under an employer-sponsored retirement plan, use the rules in this table to determine how much of your IRA contribution is tax deductible, based on your MAGI:

There are a few more finer points about the traditional IRA that will help you understand whether it’s a good tool for your goals. Here are a few, presented rapid fire:

- When do you pay taxes on a traditional IRA? The rules state that you pay taxes on earnings when you withdraw money. Withdrawals from a this type of IRA are taxed as income. So whatever your income tax rate is when you take the withdrawal is the rate at which those funds will be taxed.

- Are there penalties for early withdrawals (IRA distributions) from a traditional IRA? Yes. For this type of IRA, you will face a 10 percent penalty for taking IRA distributions before age 59½. This is on top of any taxes you’ll owe. For example, if you withdrew $1,000 before age 59½, you would pay a $100 penalty (10 percent of $1,000), plus the taxes you would pay on the $1,000 as though it were income. (There are, however, some exceptions to this rule.)

- What is a required minimum distribution (RMD)? Traditional IRAs are subject to an RMD. An RMD is an amount of money that the IRS requires you to withdraw from this type of IRA after age 70½. According to the rules, you must take your RMD by April 1 of the year following the calendar year in which you reach age 70½ and by December 31 in all subsequent years. So if you turned 70½ on December 31, 2018, you must take your RMD by April 1, 2019. If you turned 70½ on January 1, 2019, you would take your RMD by April 1, 2020. Important note: The penalty for not taking your RMD is a steep 50 percent. That means if you were supposed to take a RMD of $3,000 and failed to do so, you would owe the IRS $1,500 in addition to any taxes you owed on the distribution.

What is a Roth IRA? Rules & age requirements

The Roth IRA, named for Senator William Roth of Delaware (pull that out on trivia night!), differs from a traditional IRA primarily in its taxation rules. Contributions to a Roth IRA are made after you pay taxes, so there’s no tax deduction for your contributions. However, your investment grows tax-free and withdrawals (IRA distributions) are not taxed.

One nice benefit of this IRA type: there is no age limit on who can open or make contributions to a Roth IRA. So as long as you are working, you can continue to contribute to your Roth IRA.

Besides taxation, another difference between the Roth and traditional IRA is the rule about who can make contributions. High earners may be limited or restricted in their contributions to a Roth IRA. This table can help you determine whether your Roth IRA contribution limits are affected by your income. If you are limited because of a high income, see the section below on how to open backdoor Roth IRAs.

Most earners, though, are eligible to open this type of IRA. And there are several benefits to doing so, including these:

- Distributions are not taxed when withdrawn. Unlike traditional IRA distributions, Roth IRA distributions are not taxed when they’re withdrawn. This makes the Roth IRA an appealing investment type for younger workers. Assuming you will potentially earn more as your career advances, you will be in a higher tax bracket when you retire than when you contribute the funds. This could translate to significant tax savings.

- You can withdraw contributions tax-free at any time. That’s contributions only, not interest you’ve earned.

- Under certain circumstances, distributions from this type of IRA can be taken before retirement. Another advantage of a Roth IRA is that you can take what are called “qualified distributions” of both contributions and earnings before you retire without paying any federal taxes or a penalty for early withdrawal. A qualified distribution is one that follows both of the following two rules: first, the distribution happens at least five years after you open the Roth IRA. And second, you’re at least 59½ when you withdraw funds; OR you take out $10,000 or less to buy or rebuild a first home for yourself, your child, or your grandchild; OR you have become disabled; OR the distribution is made to your estate after your death.

- There is no required minimum distribution after age 70½. The Roth IRA rules do not require an RMD after age 70½. This means you don’t have to worry about the possibility of penalties for failing to take a distribution. This also means you can contribute to a Roth IRA for longer than you can with other IRA types. Finally, no RMD means a Roth IRA can be a vehicle for passing funds on to your heirs, though there is some debate about whether it is the best type of IRA for this.

What is a backdoor Roth IRA?

We mentioned above that there’s an upper income limit on who can open a Roth IRA: if you make too much money, this type of IRA isn’t available to you. But if you’re willing to take a few extra steps, you may be able to fund what’s sometimes called a “backdoor IRA” or a “backdoor Roth.”

The backdoor IRA became possible in 2010 when changes to tax rules removed income limits for converting a traditional IRA to a Roth IRA. So essentially, high earners who want to get in the “back door” of the Roth IRA game can do the following:

- Open and contribute to a regular IRA.

- Fill out tax form 8606 to make those contributions non-deductible.

- Convert the regular IRA to a Roth IRA. (This may be possible in as little as a few days.)

Before you leap at the chance to try the backdoor Roth IRA, though, take time to consider a couple things:

- Tax law changes. The newest overhaul took effect on January 1, 2018. As of this writing, backdoor Roth IRAs are still legal (if a little complicated) – but if you’ve got any doubts, check in with a tax accountant to make sure your strategy is within the rules.

- This may not be the best move for everyone. The backdoor IRA can offer tax savings if you’re a high earner. But it’s not right for everyone. If you’re not sure whether it might help you, do some googling or talk to your tax accountant.

SIMPLE IRA: Rules & age requirements

What is a SIMPLE IRA? First and foremost, note that SIMPLE is an acronym. A SIMPLE IRA is a Savings Incentive Match Plan for Employees IRA.

In practice, it’s a type of employer-sponsored retirement plan that lets employees contribute a portion of their pre-tax income. Employers are required to make contributions to a SIMPLE IRA by either matching their workers’ contributions or making annual contributions whether or not workers contribute.

To be eligible for a SIMPLE IRA, the rules state that you must…

- Have earned at least $5,000 in any two previous years.

- Expect to earn at least $5,000 this year.

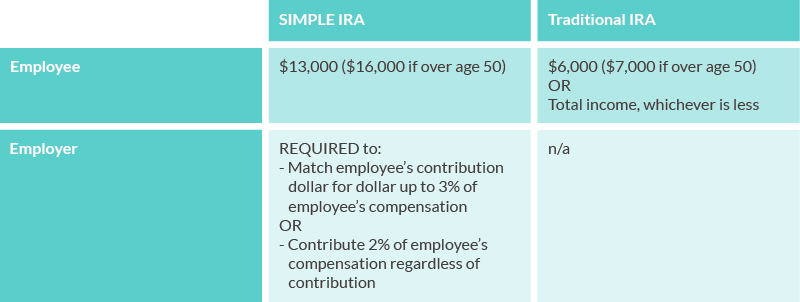

SIMPLE IRA vs. traditional IRA

The main difference between a SIMPLE IRA and a traditional IRA is that your employer has to open a SIMPLE IRA, whereas you yourself open a traditional IRA. There are also differences in IRA contribution limits between a SIMPLE and traditional IRA, as outlined below.

Finally, taxes and penalties are different for SIMPLE vs. traditional IRAs:

- Employee contributions are NOT tax-deductible for SIMPLE IRAs. (Exception: if you’re a sole proprietor, they may be.)

- If you withdraw funds early from a SIMPLE IRA within two years of your employer’s first contribution, the early-withdrawal penalty is 25 percent. After that, it’s just 10 percent (vs. a traditional IRA, where it is always 10 percent).

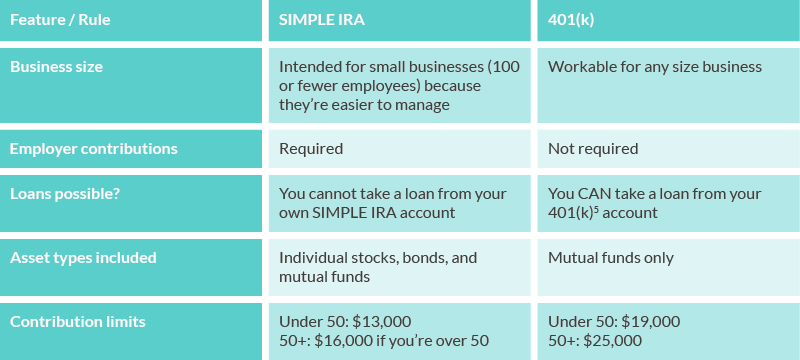

SIMPLE IRA vs. 401(k)

If you’ve ever had a 401(k), you’re probably wondering how the SIMPLE IRA is different. Here’s an overview:

So there you have it – the (anything but) SIMPLE IRA.

SEP IRA: Rules & eligibility

What is a SEP IRA (pronounced “sep,” not “s. e. p.”)? Again, we’ve got an acronym on our hands. SEP stands for Simplified Employee Pension.

This type of IRA is an employer-sponsored retirement plan. Employers are not required to contribute annually, but the rules state that for any year they do contribute, they must contribute to all eligible employees’ SEPs (in other words: no playing favorites).

If you make contributions to your SEP IRA, these count toward your combined traditional and Roth IRA contribution limit of $6,000 for the year (as of 2019). Your employer’s contributions are capped at 25 percent of your compensation, or $56,000, whichever is less.

Another consideration: employers who fund SEP IRAs must proportionally fund all eligible accounts. For this reason, this IRA type is particularly popular for sole proprietors, business owners with no employees, and freelancers. It lets them funnel a lot of money toward retirement, as their cash flow allows, without forcing them to fund anyone else’s.

We mentioned that employers must contribute to all eligible employees’ accounts any year they fund their SEP. So how is SEP IRA eligibility determined? Employees are eligible for SEP IRAs when they…

- Are 21 or older.

- Earn at least $600 for the year.

- Have worked for the employer for three out of the five years preceding the year for which the contribution is being made, regardless of how much of any given year they worked for their employer.

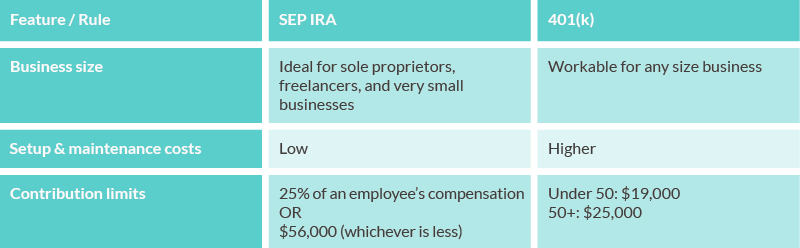

SEP IRA vs. 401(k)

Both SEP IRAs and 401(k) plans let businesses establish retirement plans for employees. There are important differences between the two, however, including these:

What is a rollover IRA?

A rollover IRA most often occurs when you switch jobs. It happens when you take funds from an employer-sponsored retirement account and roll them into a new IRA. Rolling over money into an IRA gives you a little more control over things like asset allocation.

For a complete comparison of IRA rollover rules and limitations, refer to this IRS chart.

How do I roll over a 401(k) plan to an IRA?

Actually, you can roll over more than a 401(k) to an IRA – you can roll over any qualified plan. A qualified plan is an employer-sponsored retirement plan (such as a 401(k) or its nonprofit equivalent, the 403(b) – more on these below). There are two ways to roll over a 401(k) to an IRA:

- Direct rollover: In this scenario, you ask the person in charge of administering the 401(k) at your old job (the plan administrator) to pay the funds from your qualified plan directly to your rollover IRA. No taxes are withheld from the rolled over funds in this scenario.

- 60-day rollover: Also sometimes called an “indirect rollover,” the 60-day rollover happens when the plan administrator at your old job cuts you a check for the funds in your old account and you deposit them into a new IRA within 60 days. As long as you meet the 60-day deadline, there are no tax or early-withdrawal penalties. If you don’t put the funds into a new IRA, the entire amount will be considered taxable income (i.e., you’ll have to pay taxes on it). If you’re younger than 59½ when you do this, you will also owe the 10 percent early-withdrawal penalty.

The most efficient and least tax-consequential way of rolling over a 401(k) to an IRA is to opt for the direct rollover if it’s available to you.

How do I open an IRA?

Opening an IRA is a fairly painless process and, like so many things these days, can be done completely online. Basically, the steps for opening an IRA are as follows:

- Decide which IRA provider you will use.

- Decide which type of IRA you will open (remember: the best IRA for you depends on your individual circumstances).

- Apply to open your IRA.

- Fund your IRA through a bank account or by rolling over another account.

- Choose your investments.

And voilà! You’ve opened an IRA.

How much are IRA fees?

Administrative IRA fees vary by provider. Maintenance fees can run anywhere from $25 to $100 annually – but providers will often waive those fees if you maintain a minimum balance.

If you itemize your tax deductions, there are tax rules that may let you write off your IRA fees as a miscellaneous investment expense on Schedule A of Form 1040.

What is the best IRA?

We told you – there is no best IRA!

But we get it – you still want to know. The truth is, the best IRA for one person might not be even a good IRA for someone else. The best IRA for you will depend on many factors, including:

- Your age when you open the IRA.

- Whether you’re covered under an employer-sponsored retirement plan like a 401(k).

- Your need for someone to manage the IRA investments for you or your ability and desire to handle them yourself.

- Your retirement goals.

In other words, the best IRA for a full-time employee in her 20s with access to a 401(k) who freelances on the side will almost certainly be different than the best IRA for a part-time worker in his 50s without any employer-sponsored options.

The best IRA is the one that lets you reach your retirement goals by paying as little in taxes as possible.

Want more guidance on which IRA is best? These general rules apply in many cases:

- If you freelance or own a single-person business, a SEP IRA often works well.

- If you’re a small-business owner, a SIMPLE IRA may help you encourage your employees to save for retirement.

- If you have access to a 401(k) through an employer, that’s probably a good choice, especially if the employer offers a match.

- If you expect to have higher income in retirement than you do now, a Roth IRA may make sense.

- If you expect to have lower income in retirement than you do now, a traditional IRA may make sense.

Borrowing from an IRA

Maybe you’ve heard that you can borrow from an IRA if you come across an unexpected expense. But here’s the thing: there’s no such thing as an IRA loan.

IRA rules state that you can’t use your IRA to fund a loan to yourself, and your IRA balance can’t be used as loan collateral. In fact, the IRS classifies both borrowing from an IRA and using it as collateral as “prohibited transactions” (see Publication 590-A).

This is true for all types of IRAs, including Roth IRAs.

With a Roth IRA, however, the withdrawal rules are a little more flexible. Because Roth contributions are made after you’ve already paid taxes, you can withdraw your contributions to a Roth IRA at any time without any penalty (that’s contributions only – not any interest you’ve earned on those contributions).

So let’s say you’ve contributed the maximum annual amount to a Roth IRA for seven years. You could withdraw up to that amount (but not any interest that money has earned) without paying any taxes or penalties. But that money isn’t considered borrowing from your IRA or an IRA loan: you don’t have to pay it back.

What if I inherit an IRA or a Roth IRA?

Inheriting an IRA can be tricky. The way you handle the funds from an IRA inheritance can have significant tax consequences. You have several choices of how to proceed; those choices depend largely on two factors:

- Whether you were married to the person you inherited from.

- Which type of IRA you inherited: traditional or Roth.

For a detailed discussion of what to do when you inherit an IRA, you may want to start with this blog post.

What does it mean to rebalance an IRA?

Rebalancing your IRA means buying or selling investments to make your IRA match your asset allocation. Asset allocation is the way you distribute your money among investments. Different investment types (stocks, bonds, real estate, commodities, etc.), different sectors (technology, healthcare, etc.), and different geographic regions have varying levels of risk. When you rebalance your IRA, you move money around to adjust your risk exposure.

Rebalancing an IRA is used to maintain proper “diversification.” Diversifying an IRA means including different types of investments that have different risk profiles with the goal of evening out any ups and downs caused by market fluctuations (geek speak: the investments are uncorrelated with each other). The idea is to not have all your money in any one type of investment or at any one level of risk.

Because every investor is different and every investment goal is different, there is no one rule for how to diversify. Your age (how long you have until retirement), your earning potential, how much you have to invest – consider all these factors as you decide how much and what kind of risk to take in your IRA investments.

Brokerage accounts vs. IRAs

The main difference between a brokerage account and an IRA is taxes. Anytime you sell an investment in a taxable brokerage, you create a taxable event. Depending on whether you made or lost money and how long you held the investment when you sold, you may owe income or capital gains tax. This is not true with an IRA. Funds are either taxed on their way in (Roth) or on their way out (traditional). Investments inside the IRA grow tax-free.

Another important difference: because brokerage accounts don’t have any special tax advantages, you can take money out without paying penalties. So the best choice for most investors would be to open both a brokerage account (for shorter-term savings goals) and an IRA (for retirement).

IRA vs. 401(k)

We’ve tackled the differences between various types of IRAs in the sections above. Here’s a summary of the main differences between IRAs vs. 401(k)s, which are a substantially different investment tool:

Part 2: 401(k), 403(b), and 529 Plans

Of course, not all investment types are IRAs. Here, we’ll look more closely at the 401(k) and 403(b), which are retirement accounts, as well as the 529 plan, which lets you save for education.

What is a 401(k)?

The 401(k) is named for the section of the tax code that governs it. (So it would be like if you decided to start going by 1.1-1.) A 401(k) is an employer-sponsored plan that lets you save pre-tax earnings for retirement. Your employer may or may not choose to match those funds up to a certain amount.

For example, let’s say you make $55,000 a year and your company matches up to three percent of your salary as 401(k) contributions.

Three percent of $55,000 is $1,650, so your employer will match your contributions up to that amount. If you socked away $10,000 in this scenario (and nice work if you did), the total amount added to your 401(k) by year end would be $11,650: your contribution plus your employer’s match for the first three percent of your salary.

In other words, if your employer offers a 401(k) match, it’s basically free money. Take advantage of it!

Is a 401(k) an IRA?

No. A 401(k) is not an IRA. It is an employer-sponsored retirement plan, whereas an IRA is an individual retirement account.

What are the contribution limits for a 401(k)?

In 2019, contribution limits for a traditional 401(k) are $19,000 for individuals under 50. If you are over 50, you can make a $6,000 “catch-up” contribution, for a total of $25,000. These limits are only on your contributions and do not include employer contributions. The total combined maximum contribution limit for employee and employer is $56,000 for 2019.

Who makes investment decisions for a 401(k)?

You do – sort of. Your employer and plan provider determine which mutual funds are available to you in your 401(k), and you choose from among those funds.

Many 401(k)s offer “target date” funds, which offer mutual funds that have an appropriate level of risk for various retirement dates. The risk level of these funds is adjusted as you approach retirement.

What is the difference between a 401(k) and an IRA?

The two biggest differences between a 401(k) and an IRA are…

- Contribution limits.

- Investment choices.

401(k) plans allow for much larger maximum contributions and carry the potential of employer matching. But 401(k) plans offer a much more limited selection of investment options (mutual funds only). IRAs, on the other hand, can include investments in stocks, bonds, ETFs, etc.

Roth 401(k) vs. a 401(k)

A Roth 401(k) is an employer-sponsored retirement plan that is funded with after-tax contributions. This means you don’t pay taxes when you withdraw money from your Roth 401(k) – you pay them on your income as you earn it.

This is true as long as the account is at least five years old and you’re older than 59½ when you make withdrawals (if you withdraw money before then, you may have to pay taxes plus an 10 percent early-withdrawal penalty). A Roth 401(k) is subject to RMDs after age 70½ (meaning you have to make minimum withdrawals starting at that age).

What is a 403(b)?

Though it behaves much like a 401(k), a 403(b), also named for its section in the Internal Revenue Code, can only be established by public schools or nonprofits (aka 501(c)(3) organizations).

What are the contribution limits for a 403(b)?

The contribution limits for 403(b) plans are similar to those for a 401(k) plan. This means that you may contribute up to $19,000 to a 403(b) plan in 2019 if you are younger than 50 and $25,000 if you are 50 or older.

Who makes investment decisions for a 403(b)?

As with the 401(k), you do (sort of). Again, your employer and plan provider typically offer a menu of mutual fund options you get to choose from. The choices you make, as with a 401(k), will largely depend on your risk tolerance.

403(b) vs. IRA

As with the 401(k), the primary differences between a 403(b) and an IRA are contribution limits and investment options. Contribution limits for a 403(b) are the same as those for a 401(k). Since you’re choosing from a limited menu, your investment choices are more limited than what you’ll see with an IRA.

Part 3: 529 Plan: Rules & Requirements

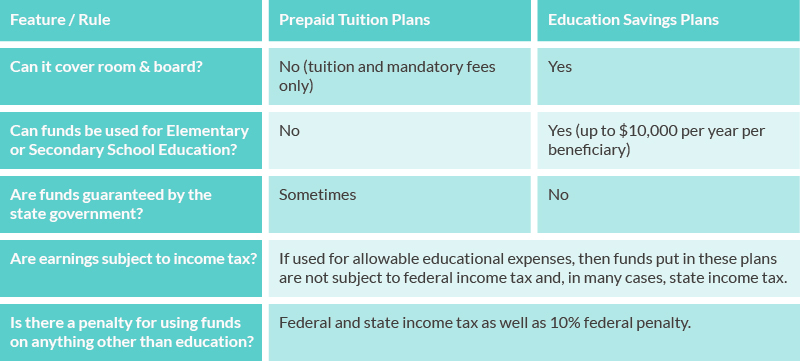

What is a 529 plan? A 529 plan, named for (say it with me) its section in the Internal Revenue Code, is a way of saving money for education costs. They fall into two categories: prepaid tuition plans and education savings plans. This table helps explain the differences between the two types of 529 plans:

529 vs. Roth IRA for saving for education expenses

When saving specifically for education expenses, there is no competition between the 529 plan and a Roth IRA – the 529 plan is the way to go. However, if you’re unsure whether you’ll actually need to use the money you’re setting aside for education, then the Roth IRA may offer some advantages, including these:

- Retirement savings: The number-one advantage of setting aside money in a Roth IRA is that you can use the funds for retirement if you don’t use them for education. This does not work the other way around without severe penalties and tax consequences.

- Tax- and penalty-free withdrawal of contributions: As we mentioned above, you can withdraw money you’ve contributed (but not earnings) at any time from a Roth IRA without tax consequences.

- Penalty-free withdrawal for higher education: Normally, you’d pay a penalty for withdrawing Roth earnings early (before the age of 59½). However, you can withdraw earnings early without paying a penalty if you’ll be using those funds for tuition for yourself, your spouse, your children, or your grandchildren.

So, while a 529 plan is still probably the best investment vehicle for saving for future education-related expenses, a Roth IRA can be used in a pinch.

Part 4: Retirement Advice for Women Investors

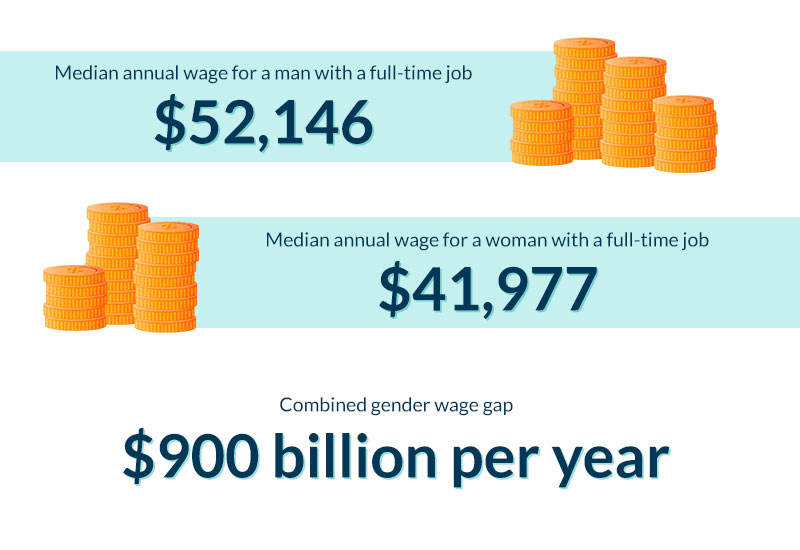

In America, there are gender differences in pay, career breaks and lifespans. On average, women will make less money over their careers and live longer. Unfortunately, these factors are not taken into account as much as they should. While women investing for retirement are just as likely to contribute to an IRA as their male coworkers, they’re 80 percent more likely to fall into poverty after age 65 and three times more likely between ages 75 and 79.

So what’s the best retirement advice for women who want to live well into their golden years? Start with these three steps:

- Save more while you’re working.

- Consider opening a spousal IRA.

- Wait longer to retire (sorry!).

Women investors need to save more

It may seem like obvious retirement advice, but saving a larger percentage of your income while you’re working is one of the best ways to address the women investors’ retirement gap.

One way to make this easier is to set up an automatic deposit. In other words, you want to make it easy to save early and save often if you’re a woman investing for retirement.

Women investors can open spousal IRAs

If your spouse continues to work for wages while you’re doing the unpaid work of caring for young children or elderly parents, a spousal IRA or spousal Roth IRA may help. These work much like individual IRAs with similar contribution limits: the working spouse contributes to an IRA on the non-working (spousal IRAs work for either gender) spouse’s behalf.

Women investors can wait to retire

The bitterest pill to swallow in terms of retirement advice for women may be the alternative of simply waiting to retire. Women can make up for some, though certainly not all, of their savings shortfall by continuing to contribute to their retirement accounts well into their 70s.

Remember, while traditional IRAs have RMDs after age 70½, Roth IRAs do not, so it’s possible to keep contributing as long as you’re earning money.

Congratulations! If you’ve read this far, you get a free IRA!

We’re not exaggerating, either: no IRA fees. Zilch. Nada. (Okay, to be fair, anyone who opens an IRA with us gets it for free. But you definitely do.)

And if you choose to open an IRA with M1, you’ll be able to take advantage of the functionalities that make our customers’ lives easier, including…

- Automatic rebalancing, which keeps your risk exposure right where you want it to be.

- Easy-to-use investing pies.

- Real human support during business hours.

- … and a lot more.

There are lots of choices to make when considering how to invest for retirement. We hope this guide has empowered you to understand some of those options. The next step is yours to take.

If you’re interested in learning how you can open an IRA or Roth IRA with M1, read all about our retirement investment options.

M1 Finance LLC is a SEC registered broker-dealer and Member FINRA / SIPC. You can check the background of M1 Finance LLC on FINRA’s BrokerCheck. SIPC protects securities customers of its members up to $500,000 (including $250,000 for claims for cash). SIPC insurance does not protect against loss in the market value of securities. Investments are not FDIC insured and may lose value. Please consider your objectives and M1 fees before investing. Past performance is not a guarantee of future results. Using margin involves risks: you can lose more than you deposit, you are subject to a margin call, and interest rates may change. Not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdiction where M1 Finance LLC is not registered.

No Recommendations or Investment Advice

You understand that M1, through the M1 Platform or any interaction you have with representatives of the firm, provides no tax, legal, estate planning, or investment advice of any kind, nor do we give advice or offer any opinion with respect to the nature, potential value or suitability of any particular securities transaction or investment strategy. You understand that you are solely responsible for all investment decisions you make regarding the transactions made in your account. You further understand that while you may be able to access market data and other financial information from the M1 Platform, the availability of such information does not constitute a recommendation to buy or sell any of the securities made available for purchase on the website (including securities appearing in any portfolios published by M1) or to engage in any investment strategy. Any investment decisions you make will be based solely on your own evaluation of your financial circumstances and investment objectives and the suitability for you of any security or any investment strategy. Any order entered using your password is yours and you are responsible for any outcome as a result of transactions that you initiate or that is initiated by any user of your account, including the possible loss of principal invested based on an investment decision you made. You understand the risks involved with transacting in the securities you maintain and that your investments will fluctuate in value, and you agree that M1 is not responsible for any losses you may incur as a result of your investment decisions and any trades made for your account.

By making information available to you on the website, M1 is not advising you to invest in any particular security or securities, or to pursue any investment strategy. Although M1 may provide tools that enable you to assess your own tolerance for risk, or otherwise assist to educate you in various ways, M1 does not determine if the tools and resources made available on the website will result in suitable investments designed to meet your particular investment needs. All investments have risks, and you are responsible for determining whether you can afford the risks of making any investment.You can see other terms of this content by visiting our Terms of Use.